Parting words from the head of GTM Research on how to unleash the future of electricity.

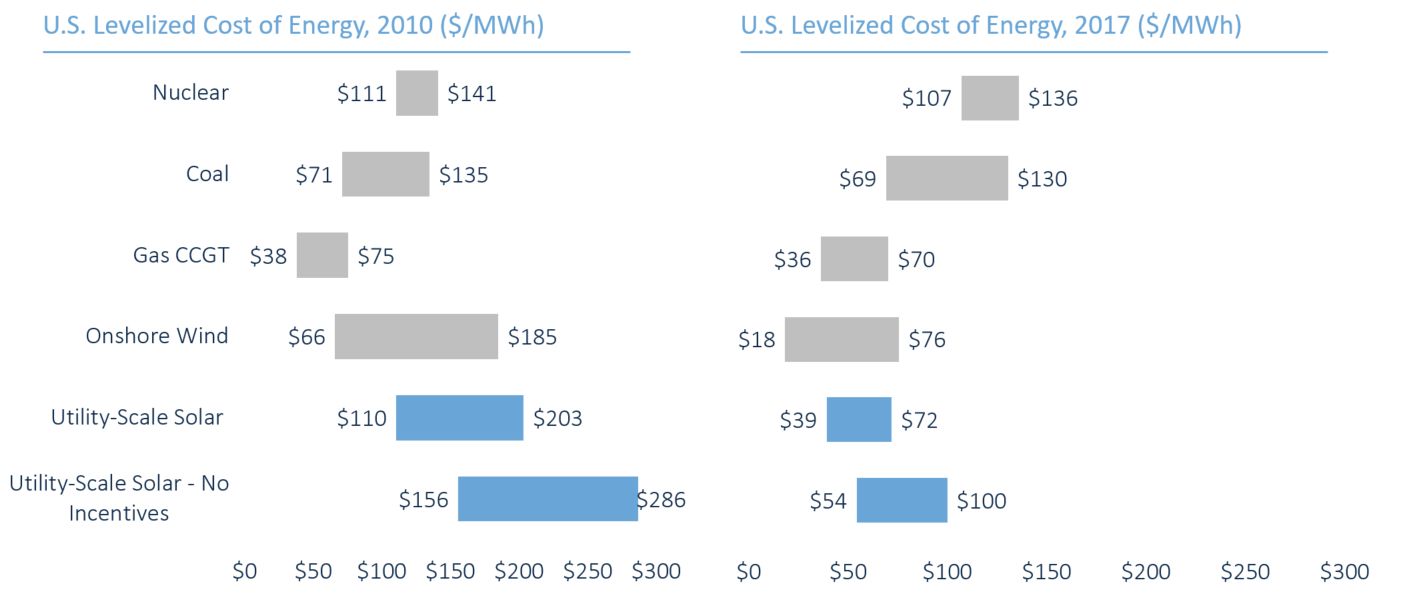

In the meantime, I’m feeling nostalgic about how much the electricity market has changed since I joined GTM in early 2009. Operating solar capacity in the U.S., for instance, has grown by a factor of 37(!). And now renewables often rank as the cheapest source of new generation capacity.

Source: GTM Research and Wood Mackenzie

Yesterday’s prevailing wisdom — that clean energy is too expensive for widespread adoption — is now rarely expressed among energy market leaders. I certainly didn’t see that changing so quickly a decade ago.

But there is a long way still to go. Today’s prevailing wisdom still assumes this transformation will pose a threat to the grid’s stability. Even if these new resources are cleaner and cheaper, surely they will impose an array of new external costs to maintain reliability and resiliency, right?

To the degree that this risk is real, it is largely self-imposed, because the next generation of energy technologies remains structurally disadvantaged in today’s power markets. Renewables, energy storage and demand response (sometimes) get credit for their potential to reduce greenhouse gas emissions, but they could offer so much more. Rather than being liabilities in tomorrow’s power system, they could be assets. But first they need the opportunity to perform.

Think of these technologies as the benchwarmers who have been spending every free minute shooting three-pointers in their backyard. Put them in the game and they’ll prove themselves stars.

Solar power can improve grid reliability

Much ink has been spilled on the challenges that higher penetrations of solar can create (in the process, teaching an entire generation of energy analysts how to draw a duck). But relatively little attention is paid to the ways solar can help stabilize the grid. A combination of smart inverters and targeted plant operation can enable solar to offer a wide array of essential reliability services, from frequency control to voltage regulation.

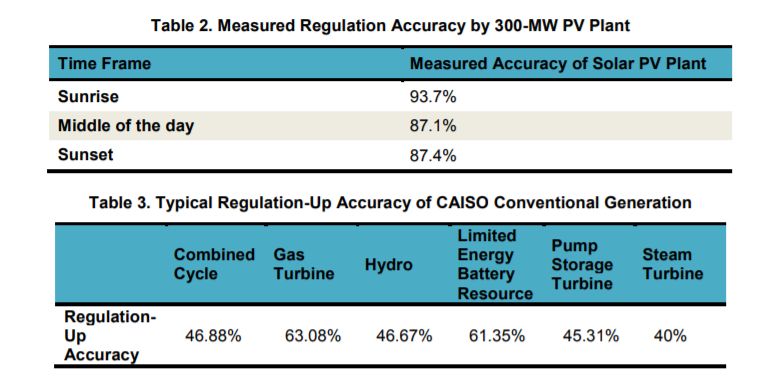

First Solar, in partnership with the California Independent System Operator and the National Renewable Energy Lab, proved this point earlier this year by strategically operating a 300-megawatt solar farm to provide reliability services to the wholesale market.

The results are impressive; not only was the project able to deliver an array of reactive power controls, but in some cases, it was able to do so better than typical gas turbine technologies.

Source: First Solar, CAISO, NREL

Did your eyes glaze over during that last section? Mine too, and I wrote it. But here is the point: First Solar demonstrated that a solar project can provide an essential reliability service better than any source of conventional generation.

But the emphasis here is on can, rather than does. The vast majority of solar projects offer no such services — not because they’re technically incapable of doing so, but because the market doesn’t reward it. Most projects are compensated purely for energy delivered (in kilowatt-hours or megawatt-hours), not for their contribution to grid reliability. And providing reliability services comes at a cost: First Solar had to curtail about 10 percent of the project’s output to leave headroom for the signal response.

To date, the solar industry’s incentive to develop advanced grid features has ben limited to either regulatory compliance or the prevention of feeder clogs and ramping issues that would hinder the installation of more solar. This has led technology providers to do everything possible to improve the cost structure of solar (and boy, have they succeeded), but relatively little to optimize the technology for grid reliability.

This is a solvable problem. Grid operators can introduce or increase incentives for reactive power, and utilities can adopt the clever model PPA developed by the Smart Electric Power Alliance to use curtailed solar as a grid resource. But first the markets need to recognize the value that solar can provide.

Microgrids can provide resilience

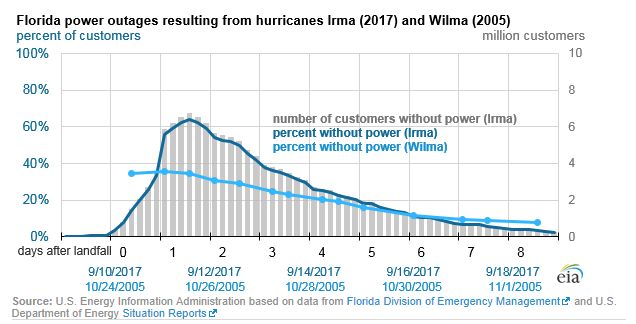

Electricity resilience is having quite a moment in the U.S. To the current administration in Washington, enhancing resilience appears to be the centerpiece of a strategy to keep baseload plants alive (and perhaps to end the “war on coal”). Meanwhile, outages in the wake of Hurricanes Harvey, Irma, Jose and Maria have tested the resilience of the grid in the Southeast U.S. and the Caribbean.

First, let me repeat a point that many others have made: resilience and reliability are different. Reliability is the ability of the grid to deliver electricity consistently when demanded. If the lights nearly always turn on when you flip the switch, you have reliability. Resilience is the ability of the grid to recover quickly and effectively from a major event (like, say, a hurricane). You can have a grid that is generally reliable but completely falls apart after a disaster, or one that is hardened to handle major incidents but experiences daily blackouts.

When a crisis incident occurs, a resilient grid offers two benefits: a smaller impact and a faster recovery. On the latter point, a variety of recent advancements have enabled faster recovery in the mainland U.S., as evidenced by the impressive recovery in Florida after Hurricane Irma.

But how about keeping the lights on in the first place? For critical facilities such as hospitals, nursing homes, police/fire stations and others, this can be a matter of life and death.

This is the sweet spot for microgrids, which are networks of distributed energy sources and loads that can operate in parallel with, or islanded from, the central grid. And there are many examples of microgrids performing handsomely during grid outages, from the chain of H-E-B supermarkets in Texas that used microgrids to keep operating during Hurricane Harvey to the Princeton University microgrid that maintained power during Hurricane Sandy. (As a side note, not to brag on behalf of the sector, but solar performed well during Hurricane Harvey and energy storage did just fine during Irma and Maria).

Given their cost, microgrids are not a universal solution. But they are important to have in the resilience toolbox, especially for critical facilities. A 90-day supply of coal offers little support when the T&D network is compromised (the cause of the majority of customer outages), but a microgrid can still save the day.

However, two regulatory barriers continue to hinder the expansion of microgrids.

- Utility franchise rights: Selling power to third parties via new distribution lines infringes on utility franchise rights, the generally exclusive agreement between the utility and a municipality to use public rights-of-way for lines and wires. This prevents the development of larger-scale microgrids that may be more economic, or could provide benefits to a larger customer group.

- Threat of public utility regulation: Any entity that sells energy or power and whose equipment crosses a public street is defined as an electric corporation that falls under the traditional utility regulation and ratemaking authority of the public utility commission. The prospect of being treated as a traditional utility shifts additional burdens onto third-party microgrid providers, making it more difficult to achieve economic viability.

This, too, is a solvable problem. Regulators can place legal guardrails around the introduction of microgrids that could allow them to proliferate without undermining the nature of our regulated utility monopolies.

Energy storage can serve as peak capacity

Depending on who you ask, energy storage is either the power grid’s Swiss army knife or its bacon. Either way, it’s versatile. Rocky Mountain Institute did great work two years ago by identifying 13 individual services that batteries can provide to the grid, utilities and customers.

But in reality, the energy storage projects operating today offer a very limited subset of those services, and the rest remain largely out of reach because markets haven’t yet adequately adapted.

Take the grid’s need to ensure sufficient peak capacity. This is a perfect fit for batteries — peak periods are rare but require fast response from flexible resources. A battery can be called upon occasionally to mitigate peak generation needs while being more regularly cycled to serve another value stream such as demand-charge reduction for a commercial customer. Such value-stacking can reduce the cost to consumers of meeting peak requirements and displace what would otherwise certainly be a rarely used, GHG-emitting plant.

Recognition of this potential is spreading.

- In California, state officials have essentially canceled plans for a 262-megawatt gas peaker after discovering that a portfolio of energy storage (mixed in with some solar and demand response) could provide the same technical capabilities and potentially at a competitive cost.

- In both California and Washington, policymakers and regulators have issued orders forcing utilities to consider energy storage to meet peak demand.

But where we haven’t yet seen energy storage take hold is in wholesale capacity markets, where grid operators procure resources to ensure adequate power supply in the future. These capacity markets are huge — GTM Research analysis earlier this year estimated that $14 billion went through these markets in the 2015/2016 delivery year. If energy storage were to gain a 10 percent share, this would open up roughly 30 gigawatts of demand for batteries — around 50 times today’s total capacity.

This is a perfect example of markets struggling to keep up with technology. Energy storage is generally allowed to participate in capacity markets in principle, but is effectively barred from doing so because market rules, ranging from performance requirements to combined resources, haven’t been updated with the unique characteristics of batteries in mind.

FERC, which regulates the wholesale market operators, took steps toward fixing this problem in 2016 by issuing a notice of proposed rulemaking (NOPR) that would have forced system operators to redesign their rules to account for these new resources. But that rulemaking has stalled under the new administration, and FERC currently seems preoccupied with another NOPR aimed at saving baseload plants.

Energy storage doesn’t need big subsidies. It just needs to be eligible to compete.

Distributed energy resources can defer or eliminate the need for grid upgrades

U.S. utilities spend over $40 billion each year to upgrade their transmission and distribution systems, and the cost is increasing. Some of these upgrades are necessary and unavoidable, but many of them could also be cost-effectively avoided, or at least deferred, with non-wires alternatives (NWAs) — non-traditional utility investments made in lieu of a typical upgrade, often involving a combination of demand flexibility, distributed generation and energy storage.

- Our team at GTM Research has identified 133 NWA projects in the U.S. totaling nearly 2 gigawatts of capacity.

- Of these, 100 are in the planning stage, and 95 percent come from four states: New York, Oregon, Vermont and California.

Impressive though that is, it absolutely pales in comparison to the opportunity.

If a non-wires alternative can provide the same service to the grid at a lower cost than a traditional T&D investment, it should be adopted. It’s that simple. But the NWA market is held back both by regulators, who mostly haven’t yet recognized the market’s potential, and utilities, which have little incentive to procure NWAs instead of earning their regulated rate of return on a traditional capital expenditure.

Even outside the realm of NWAs, distributed energy is often restrained from providing its true value. In Texas’ ERCOT grid territory, for example, distributed energy resources are compensated based on their placement in one of four state load zones. But if these resources were priced at the local level (using locational marginal prices), they could help relieve local network congestion. This idea that was floated by ERCOT in 2015 but never acted upon.

Electric vehicles can enable greater renewable energy penetration

The coming wave of electric vehicles could be the electric grid’s best friend or worst enemy. It all depends on how the vehicle batteries are charged and discharged. EVs pull a lot of power; a typical home EV charging station will have a larger peak load than the home itself. Without proper incentives, electric vehicles will increase system peak demand, which would necessitate costly new infrastructure and potentially increase emissions.

But with smart time-of-use EV electricity rates, customers can be incentivized to charge their vehicles when power is cheap and abundant — say, in the middle of the day in markets with a lot of solar. This can serve both to avoid overgeneration and curtailment when renewables grow, and to mitigate the ramp requirement to meet the evening peak.

Evidence suggests that time-of-use rates work for this purpose. San Diego Gas & Electric showed success through a multi-year experimental study with EV owners in its territory. Not only did customers respond effectively to price signals by charging their vehicles during off-peak and super off-peak hours, but they did so increasingly over time.

Electric vehicles can also offer a multitude of benefits to the grid and to utilities, well beyond renewable integration. But the EVs on the road today rarely provide those benefits.

Utilities and regulators can lock in the benefits of vehicle electrification through a combination of smart rate structures and strategic investment in charging infrastructure. But as Rocky Mountain Institute points out in this fantastic new paper, with 30 percent to 40 percent annual growth in EV sales, there is no time to waste.

It’s only going to become more challenging

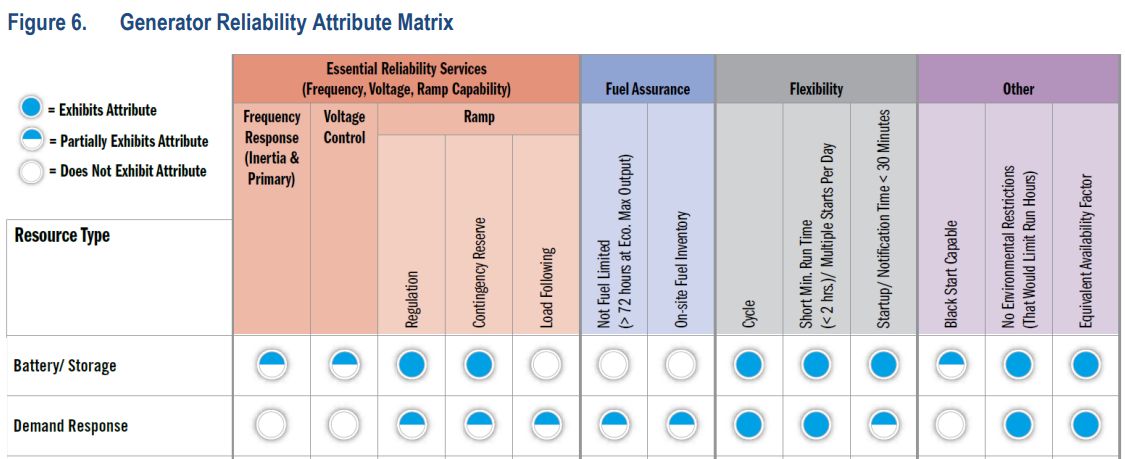

As new energy technologies converge, both the opportunity and the market design complexity will rise. Demand response is a great example of this. While well understood for its potential to respond to critical “events,” technology combinations are enabling demand response to provide much more value.

In particular, the combination of battery storage and demand response offers at least the partial ability to provide every reliability attribute that mid-Atlantic grid operator PJM has identified:

Source: PJM

Or, to take another step, consider what will happen once blockchain applications for energy begin to proliferate. Regulators will need to grapple not only with the nuances of valuing and compensating distributed energy resources, but also potentially with peer-to-peer trading, customer exposure to wholesale prices, or even the complete disintermediation of electricity market makers.

Whaddya gonna do about it? An eight-point plan

Everything I’ve mentioned is already happening, but mostly at pilot or limited scale. Pilot projects are great — until they’re not. My biggest fear for the future of electricity is that these technologies and services remain in eternal pilot limbo because markets never evolve to unleash their potential.

It’s not too late. Here are some general rules that can help unlock the next-generation electricity system.

- Design time-variable, location-based, cost-reflective rate structures. Begin with opt-in structures for customers with on-site generation, storage or load control, but eventually roll these smart rates out to all customers.

- Score every wholesale energy market (for energy, capacity and ancillary services) according to its allowance for equal participation from individual and aggregated nontraditional resources. Amend as necessary.

- Allow utilities to earn a return on the purchase of services from these alternatives, similar to what was proposed by California PUC Commissioner Mike Florio last year. (The carrot.)

- Force utilities to consider and solicit bids for DERs and non-wires alternatives before making any major grid upgrade. If an alternative solution is equally effective and more affordable, it should win. (The stick.)

- Reward reliability and resiliency according to actual proven system requirements in a technology-agnostic manner (as opposed to arbitrarily propping up any generator with a 90-day fuel supply on hand, as proposed by Energy Secretary Rick Perry).

- Avoid the “valley of pilot death”: Before approving any pilot program, create a clear set of standards which, if achieved in the pilot, will trigger a broad rollout.

- Make every effort to rely upon up-to-date cost and performance data when considering new technologies. If the most recent public cost data is more than three months old, solicit new price quotes from market participants.

- Treat climate-change mitigation as a central component of system planning, not a “policy case” to be considered, or a term to be scrubbed, for heaven’s sake.

Applying these rules will both accelerate the energy transition and ensure that the lights stay on in the meantime. It will be challenging, to be sure. But what’s the cost of freedom?